Post # 1: “Decision to File”

As the October 15, 2020 tax-filing extension deadline approached, I was also in the middle of a divorce—meaning the 2019 return wasn’t just a routine filing. It was a shared financial item that needed a clear plan, because any refund or tax impact would affect how assets and liabilities were handled in the divorce.

The approach we agreed to—through counsel and consistent with how we had handled taxes before—was straightforward: file a joint 2019 return, and treat any resulting refund or tax outcome as part of the marital accounting to be distributed appropriately. I relied on that plan because it was practical, it aligned with prior years, and it was the least likely to create new conflict while the divorce was being finalized.

At the same time, the divorce paperwork included language recognizing that a different filing approach could potentially apply only if certain conditions were met—specifically, that any alternate status would need to be qualified and supported by outside professional review. I’m not asking anyone to take a side in a divorce case; I’m pointing to this only because it matters for what happened next: it shows the tax filing wasn’t supposed to be improvised or changed casually, and that there were guardrails around any departure from the agreed plan.

So, following the agreed approach, I prepared and filed the 2019 joint return using TurboTax (as I had done in prior years) in October 2020 (insert exact e-file/acceptance date here: ________). At the time, this felt like the responsible and settled way to handle it.

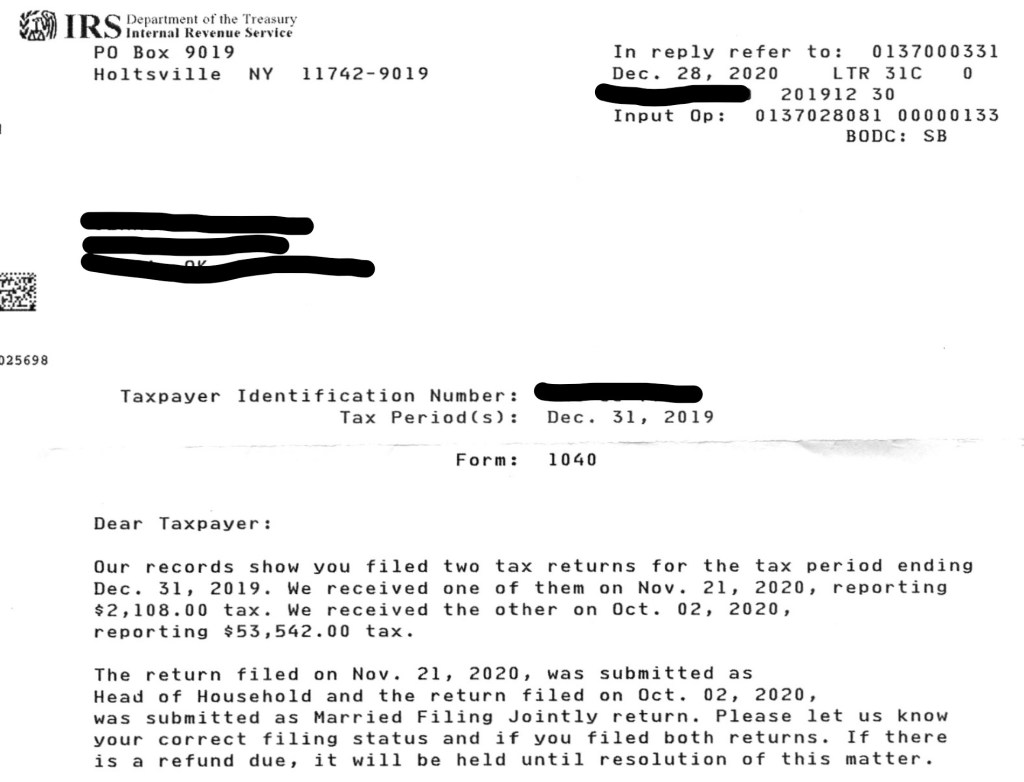

What I didn’t know then—and what became the spark for everything that followed—is that a second, conflicting return would later enter the system. That conflict triggered the IRS to acknowledge two returns had been received for the same year, and it set off the chain of events that ultimately led to the disputed IRS determination and collection action from Internal Revenue Service.

Post # 2: “Following the Court’s Order”

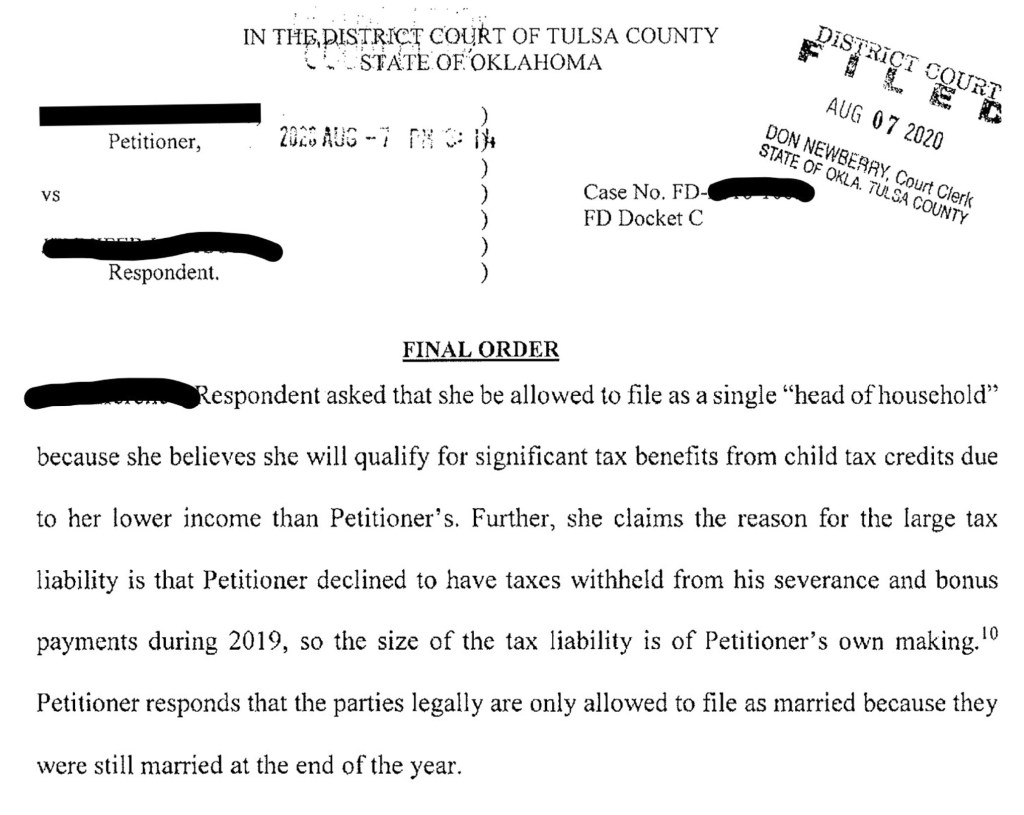

Before the IRS dispute ever started, the 2019 tax return became part of an ongoing divorce case. One key issue raised in court was whether my ex-wife should be allowed to file as “head of household” because she believed she could qualify for significant tax benefits (including child tax credits) due to her lower income. The order also reflects my response at the time—that we were still married at year-end and the filing decision needed to follow the law, not assumptions. (Attached: redacted excerpt of the court order.)

The Court made something very clear: it would not decide tax law or estimate tax differences between filing statuses. Instead, it set a process. The Court noted that the 2019 filing deadline had passed, but if the parties had not yet filed, my ex-wife would be permitted to consult an independent tax expert within 30 days. If that expert determined she could legally file in a status that allowed her to claim the benefits she expected, she could file that way. Failing that, the Court directed that the parties file jointly to achieve the least tax liability.

That framework matters because it explains the good-faith basis for what happened next: the default path under the order was a joint return unless an independent expert confirmed a different filing status was legally available. In the next post, I’ll show the milestone that followed this order—my filing of the 2019 joint return under the extension deadline—because that establishes the baseline return that was filed first, before the IRS later acknowledged receiving a second, conflicting return.

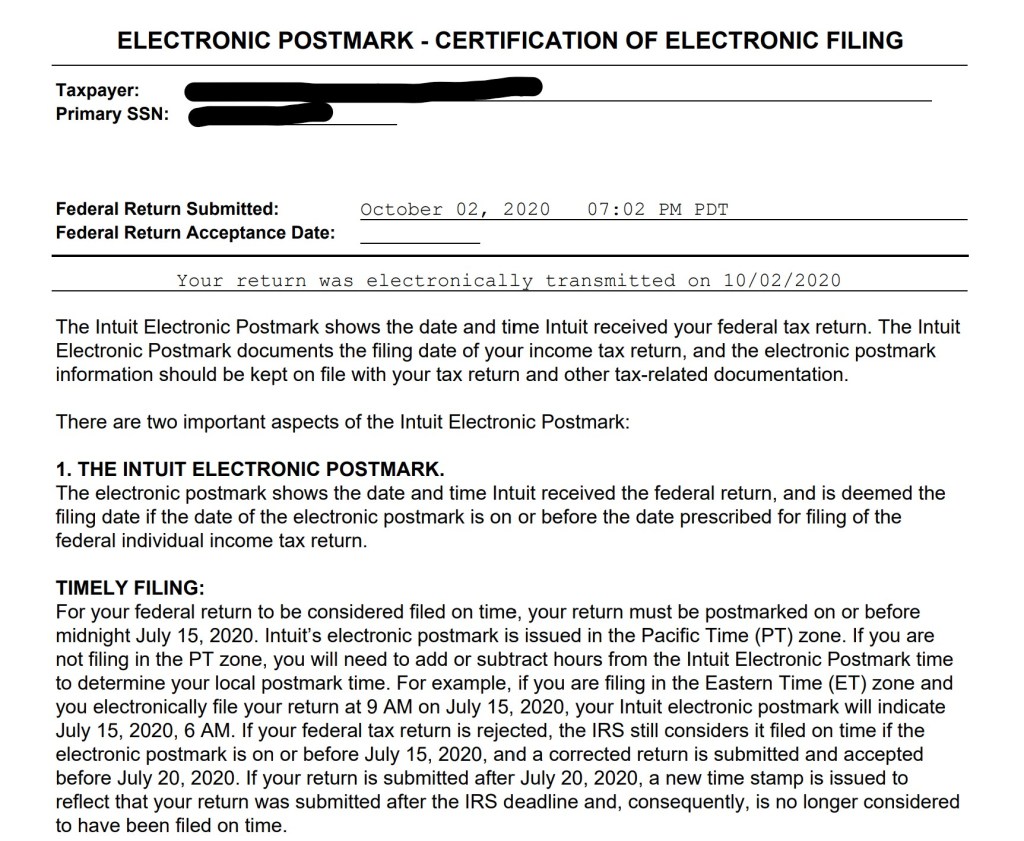

Post # 3: “The Joint Return Was Filed First (MFJ)”

After the court laid out a clear framework for how the 2019 return should be handled, the practical path was to file in the way that achieved the least overall tax liability unless an independent tax expert confirmed an alternative filing status was legally available. Based on that understanding—and consistent with how we had filed in prior years—I proceeded with a Married Filing Joint return for 2019.

Using TurboTax, I filed the joint 2019 return under the extension timeline in October 2020. At the time, this was the cleanest and most responsible approach: it met the deadline, aligned with the court-directed objective to minimize liability, and preserved the tax outcome to be handled appropriately within the divorce process.

This matters because it establishes the baseline: a valid joint return was submitted first. What happened next—and what triggered everything that followed—is that a second, conflicting return later entered the system and created a duplicate-return situation that the IRS itself acknowledged. In the next post, I’ll walk through how the second return appeared and why that single event opened the door to the IRS reclassifying the filing status and issuing the disputed bill.

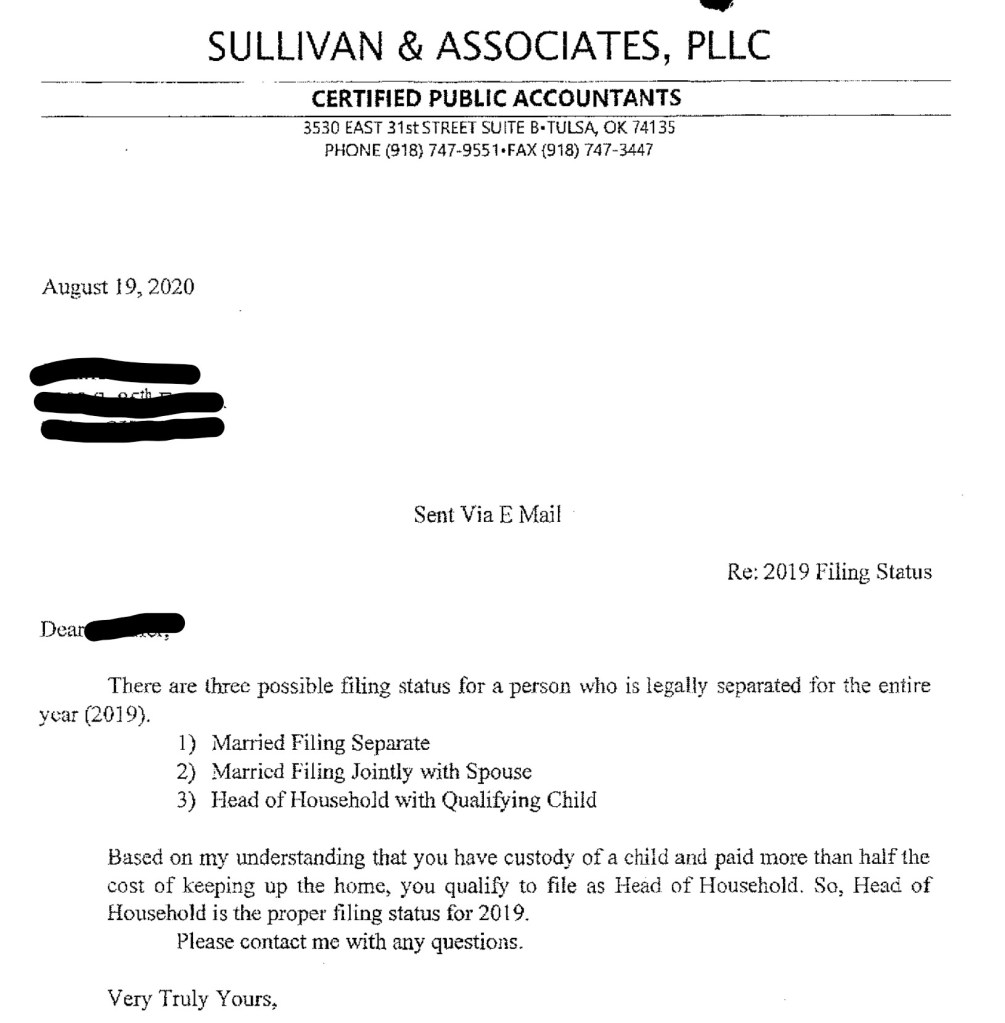

Post # 4: “The CPA Letter that Sets the Stage”

After the court order laid out a framework for how the 2019 return should be handled, the next key development was a letter prepared by a CPA that focused on the requirements for filing as Head of Household (HOH). This letter did not state that HOH was automatically available or guaranteed—it primarily described the criteria that must be met under IRS rules.

I’m sharing this letter because it became a major reference point in what happened next. HOH isn’t just a label; it comes with specific eligibility requirements tied to household support and other conditions. When someone frames a filing decision around those requirements—especially in the middle of a divorce timeline—it can create a path toward a different filing position than what had previously been planned or assumed.

For now, I’m keeping this post narrowly focused and fact-based: this is the document that explains the HOH rules that later became central to the dispute. In a later post, I’ll compare these stated requirements to the underlying facts and to the IRS’s own published guidance—because that’s where the conflict becomes clear.

Post # 5: “My Formal Response to the IRS (Sent Feb 15, 2022) “

When the IRS opened a correspondence examination on my 2019 return, I responded in writing on February 15, 2022 with a structured, document-backed packet. I’m sharing this response because it shows I didn’t ignore the issue or send a vague complaint—I provided context, evidence, and a clear request for a fair review based on the IRS’s own published guidance.

In my response, I explained that the 2019 filing was occurring during a high-conflict divorce and that many of the relevant records were court filings and attorney communications. I also stated my goal plainly: to provide as many facts as possible up front to reduce back-and-forth and avoid decisions being made on assumptions. I requested that if my submission was not sufficient, the IRS provide specific reasons and standards supporting any conclusion before finalizing an outcome.

I then addressed the key dispute points in an organized way, including:

- Why a joint return was the correct baseline filing position for 2019 under the circumstances described.

- How filing-status requirements (including Head of Household criteria) are defined in IRS guidance and how the factual record aligns with those requirements.

- A set of supporting documents intended to demonstrate consent/history of filing approach and the underlying factual record (divorce timeline items, supporting worksheets, and related exhibits).

Post # 6: “IRS Response and Proposed Changes “

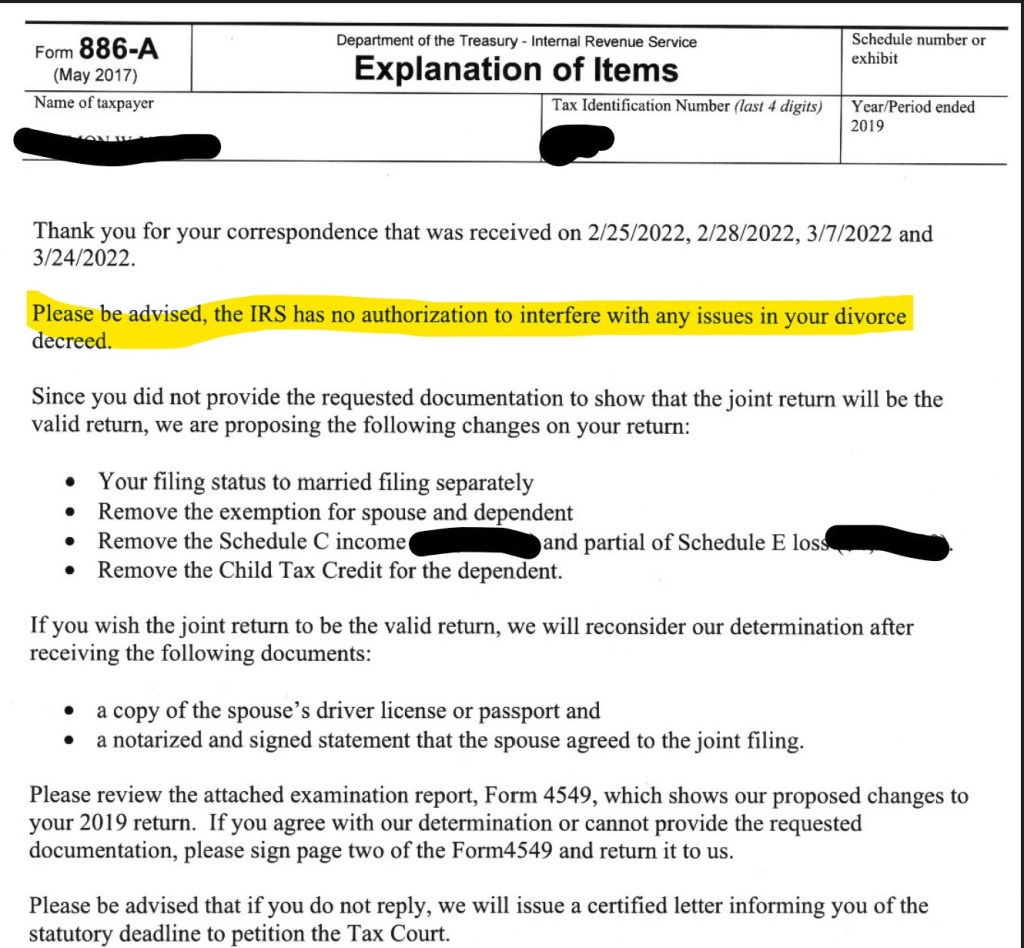

After I submitted my written response, the Internal Revenue Service issued a formal “Explanation of Items” (Form 886-A) dated 04/04/2022 that summarized what they said they received from me and what they proposed to change on my 2019 return.

They acknowledged receiving correspondence on 2/25/2022, 2/28/2022, 3/7/2022, and 3/24/2022. They stated they have no authorization to interfere with issues in a divorce decree.

They said I did not provide the specific documentation they requested to treat the joint return as the valid return, and they proposed changes including: changing filing status to Married Filing Separately, removing exemptions for spouse/dependent,removing certain reported income/loss items (as listed in the notice), and removing the Child Tax Credit for the dependent.

What the IRS said they would need to “reconsider” the joint return as valid: A copy of the spouse’s driver’s license or passport, and a notarized, signed statement that the spouse agreed to the joint filing.

They also referenced an attached examination report (Form 4549) and indicated that if I didn’t reply, they would issue a certified letter explaining the statutory deadline to petition the Tax Court.

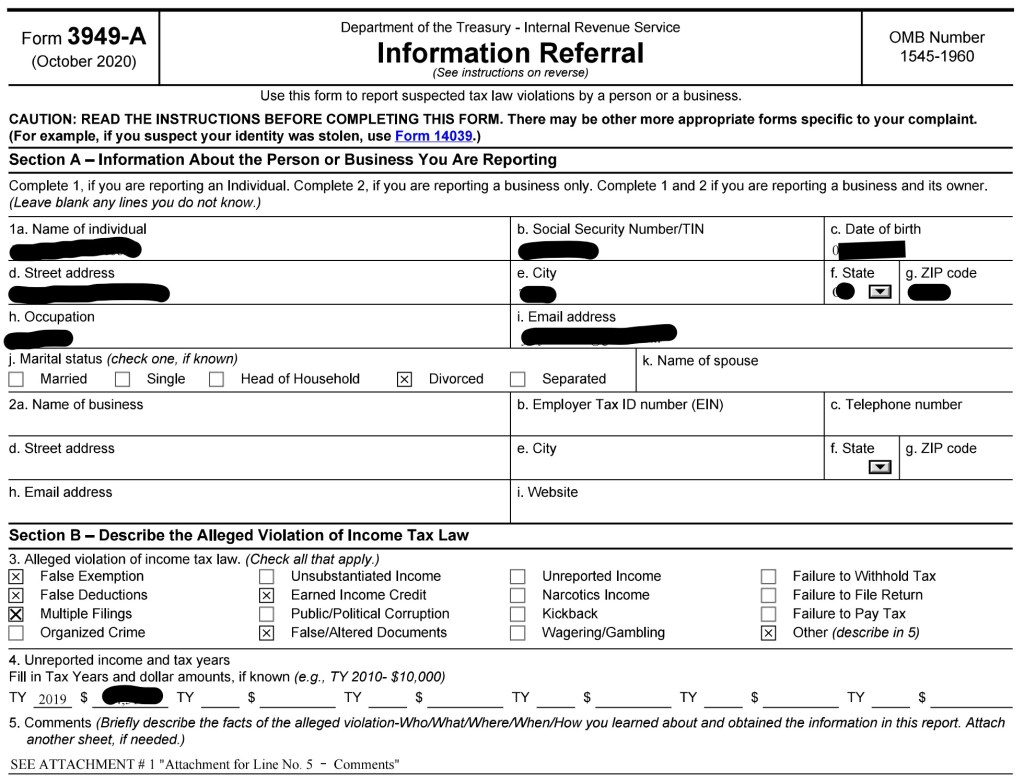

Post # 7: “Reporting the Conflicting Return to the IRS”

As I tried to get the IRS to focus on the core problem—two different returns for the same year—I also sought outside guidance on the most effective way to correct the record. After speaking with multiple tax professionals, I was advised that one practical step is to formally refer the issue to the IRS as a suspected improper filing, so the IRS evaluates the conflicting return directly rather than treating the situation as if it’s only a dispute about my return.

Based on that guidance, I submitted an IRS Information Referral (Form 3949-A). This form is used to report suspected violations of tax law and to provide the IRS with the key facts and supporting context so it can decide whether the issue warrants review. To be clear and fair: submitting this form is not a “verdict” on anyone—it’s a documented way to ask the IRS to examine the conflicting filing and the information surrounding it.

I’m sharing this step because it shows I’ve been trying to resolve this through established channels, using the procedures the IRS provides, while keeping my submissions organized and evidence-based.

Post # 8: “IRS Response Cites the Divorce Decree “

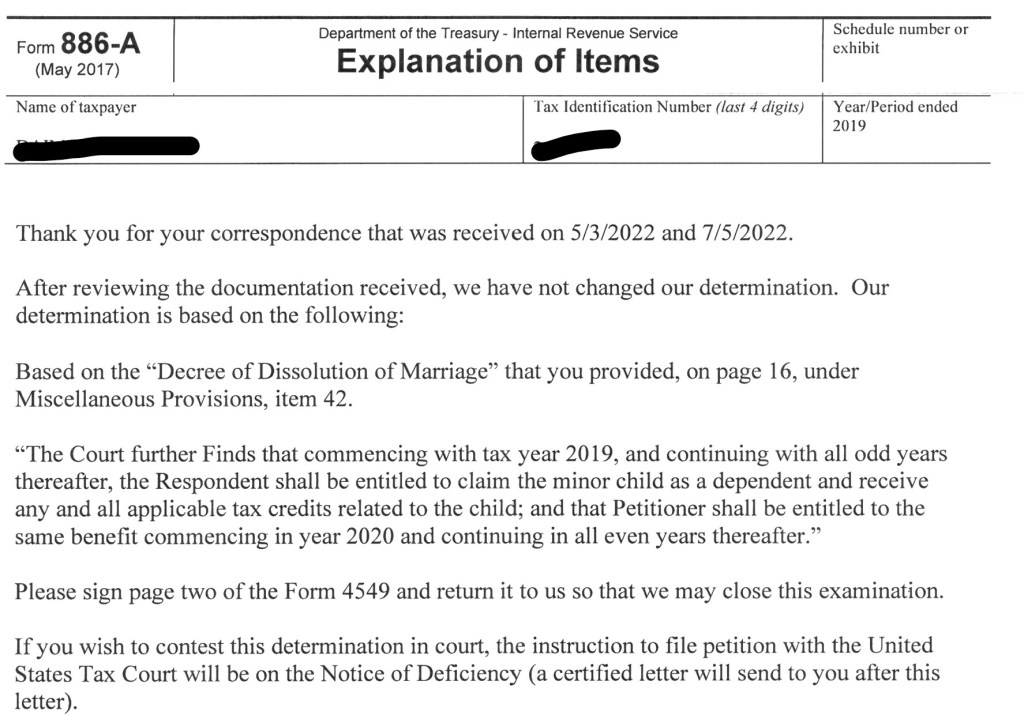

On 09/06/2022, the Internal Revenue Service issued another “Explanation of Items” (Form 886-A) in response to my ongoing correspondence. In this letter, the IRS acknowledged receiving additional documentation on 05/03/2022 and 07/05/2022, but stated they did not change their determination.

What the IRS said (facts only): They reviewed the documentation received and kept the same determination. They stated their determination was based on the “Decree of Dissolution of Marriage” I provided, citing a specific section (page and item reference). They quoted language from the decree about which parent is entitled to claim the child as a dependent and related tax credits for certain years. They instructed me to sign and return Form 4549 to close the examination and noted that if I wanted to contest the determination in court, instructions would come with a Notice of Deficiency (certified letter).

Why this matters (and why I’m flagging it): Earlier in this process, the IRS stated it was not authorized to interfere with issues in a divorce decree. This 09/06/2022 letter is important because it appears to rely on the divorce decree as a primary basis for the IRS’s determination. I’m sharing it because it shows the core tension I’ve been trying to address: what documents the IRS says it can rely on, and how that reliance affects filing status, dependency claims, and credits.

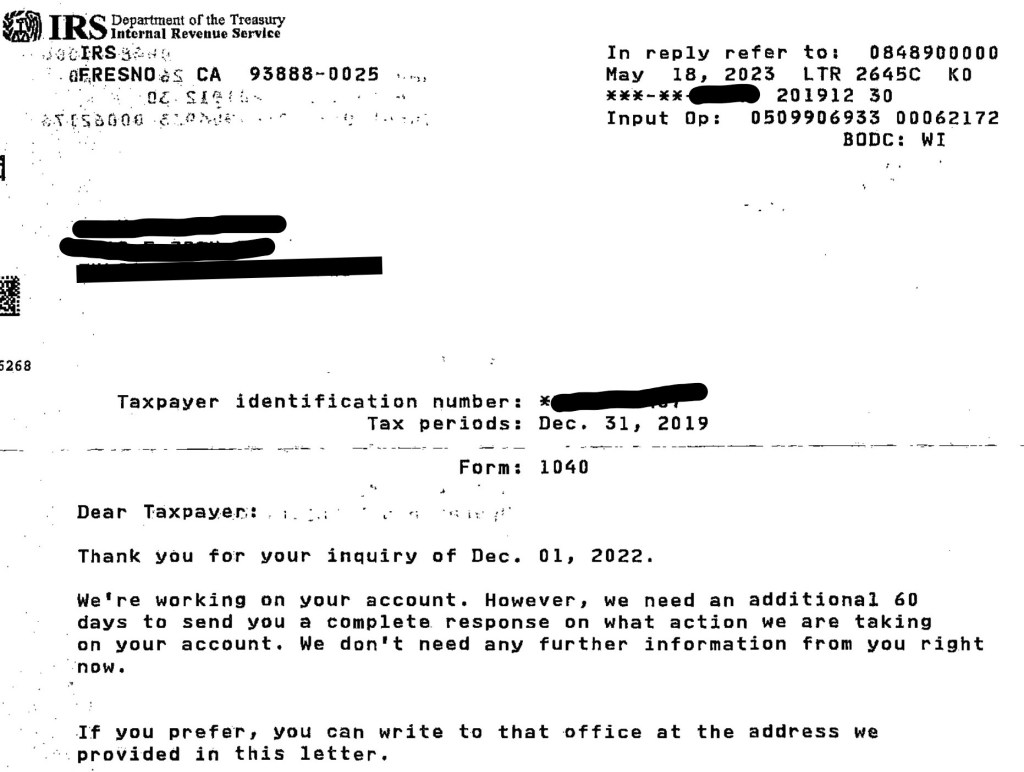

Post # 9: “More Time, Then Silence (Until They Took My Refund)”

After the IRS issued a response citing my divorce decree, I wrote back with a simple point: federal tax law controls federal tax liability, and state court orders can’t override the Internal Revenue Code. I also noted that for divorced parents, Treasury Regulation § 1.152-4 requires Form 8332 when one parent is transferring the dependency claim.

Shortly after that, I received a letter from the IRS saying they needed additional time to review my account and that they didn’t need anything else from me at that moment.

Then… nothing. I didn’t receive any meaningful follow-up for a long stretch—until I filed a later-year return and the IRS applied my refund to the 2019 balance. That refund offset forced me to re-engage the IRS again.

At that point, I submitted a formal Audit Reconsideration package disputing the IRS’s reclassification for 2019—using Form 12661 and a structured set of attachments/exhibits—specifically disputing the override of an accepted Married Filing Jointly return based on a later-filed return and reliance on a state divorce decree, and requesting the matter be routed to Appeals or handled via a local in-person review.