This page is the redacted document library supporting the Timeline and Case Overview on this website. I’m sharing documents so readers can follow the record based on dates, notices, and written submissions—not just opinions.

All documents posted here are redacted to remove personal identifiers (SSNs/tax IDs, addresses, phone numbers, account numbers, signatures, and any information that could identify a minor). I redact for privacy, but I do not change the substance of what the documents say.

Quick Start (If you only read a few items)

If you only have 3 minutes, start with these sections in order:

- IRS letters that triggered the issue (duplicate return / examination start)

- IRS determination and examination changes (what the IRS proposed/decided and why)

- Collections escalation (why the situation is urgent)

- My reconsideration submission (what I filed to request correction)

A) IRS Letters & Examination Documents

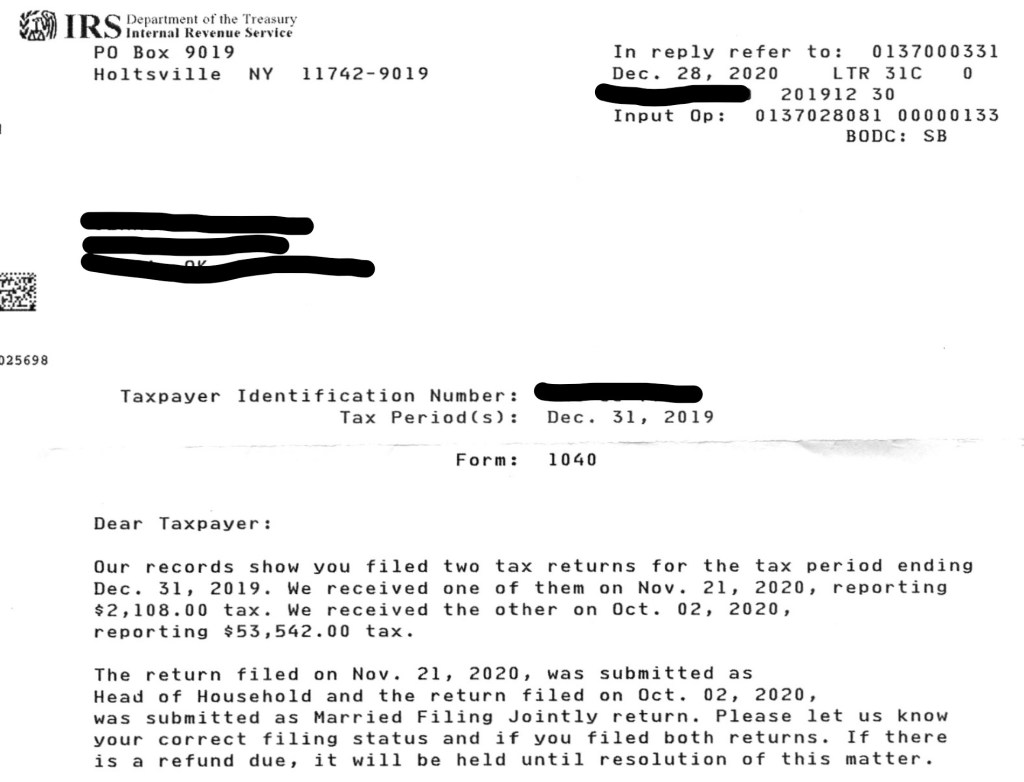

What it shows: The IRS identifies that more than one return was received for the same tax year.

Why it matters: This is the trigger that turns a normal filing into a formal IRS conflict that must be resolved.

1) IRS “Duplicate Return” Letter (Two Returns Received)

These are the IRS-issued documents that define what the IRS reviewed, what changes were proposed, and what the IRS said it relied on.

2) IRS Examination Start Letter + Explanation of Items (Form 886-A referenced)

What it shows: The IRS opens the correspondence examination and frames the issues under review.

Why it matters: This begins the documented administrative record and sets the rules for how the dispute proceeds.

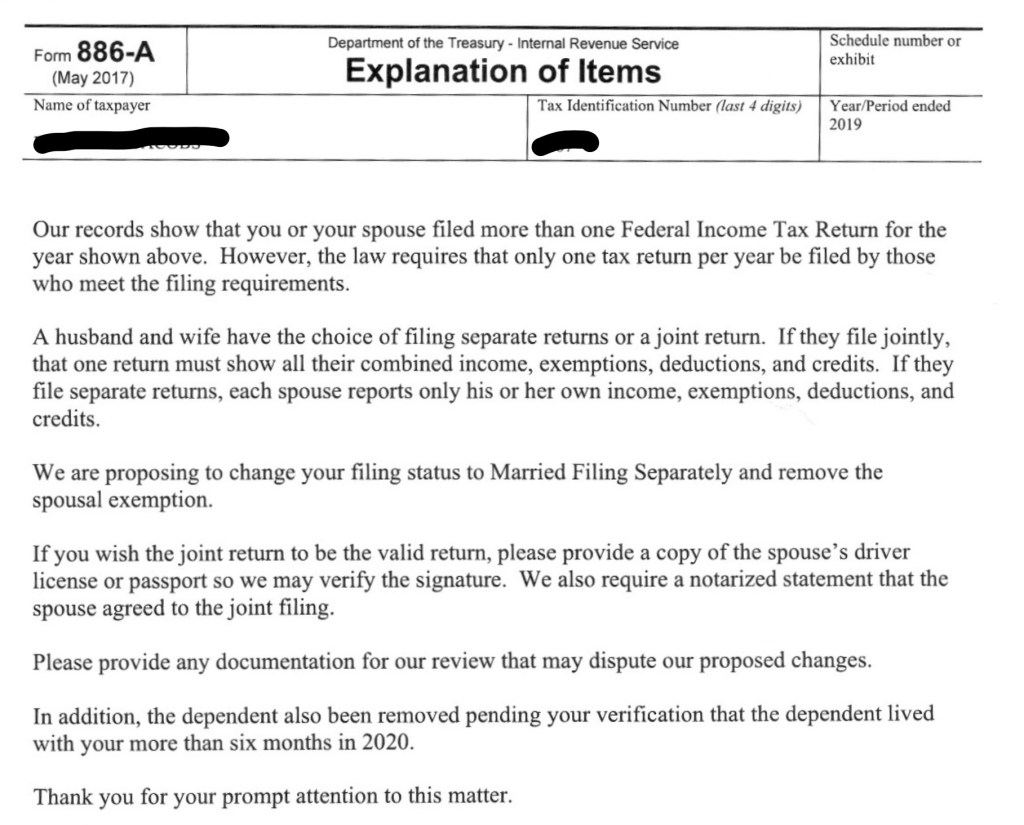

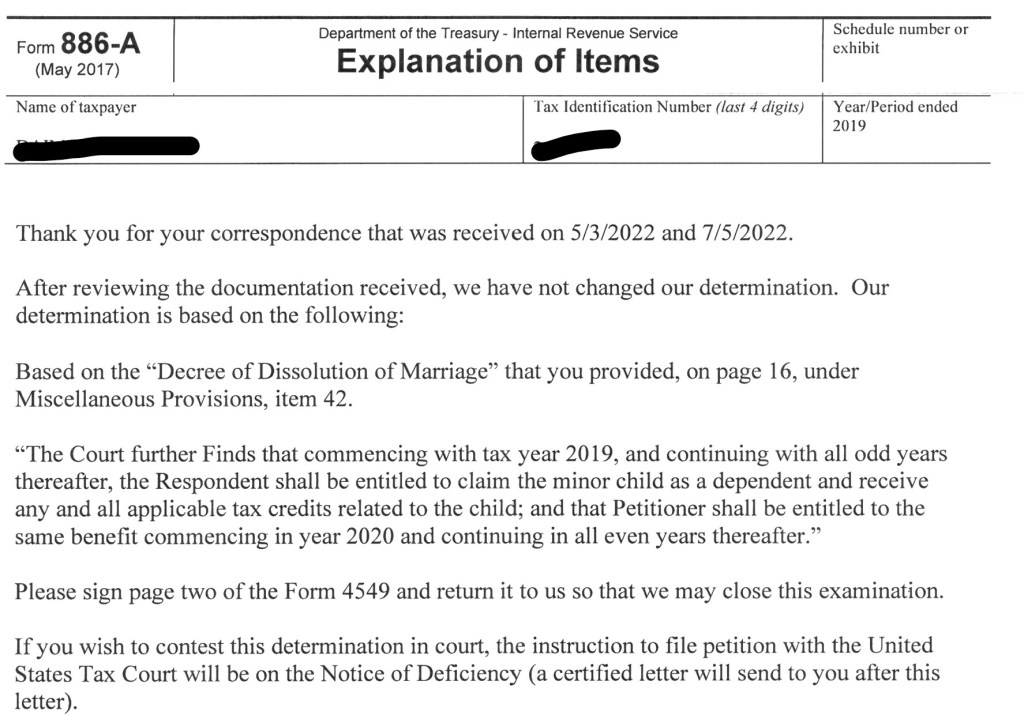

3) IRS “Explanation of Items” (Form 886-A) — Proposed Changes (04/2022)

What it shows: The IRS proposes specific adjustments and lists what they say they need to “reconsider” the joint return.

Why it matters: This is where the IRS position becomes concrete and the financial consequences start to take shape.

Note: The IRS’s position that they have no authorization to interfere with any issues in the divorce decreed, however you will see later they based their finding on the divorce decree.

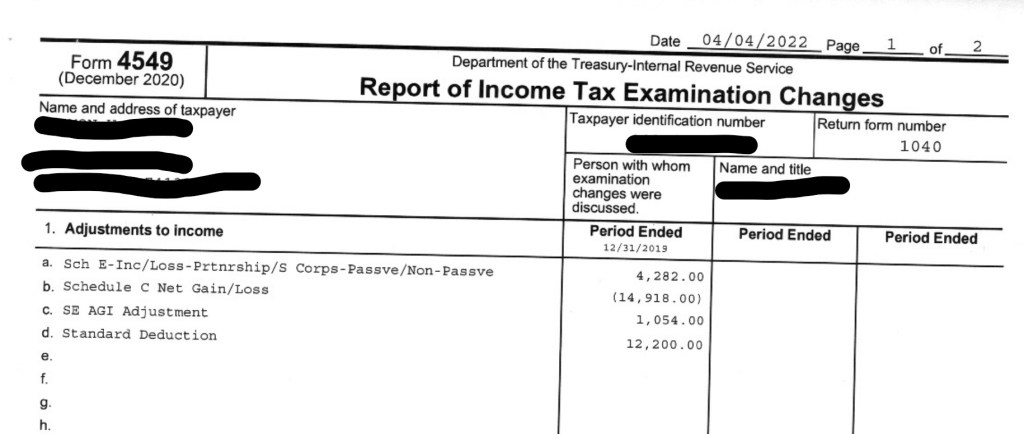

4) IRS Examination Changes (Form 4549 / related exam report)

What it shows: The IRS’s examination calculations and the proposed changes to the return.

Why it matters: This is the technical backbone of the IRS adjustment and the starting point for formal disagreement.

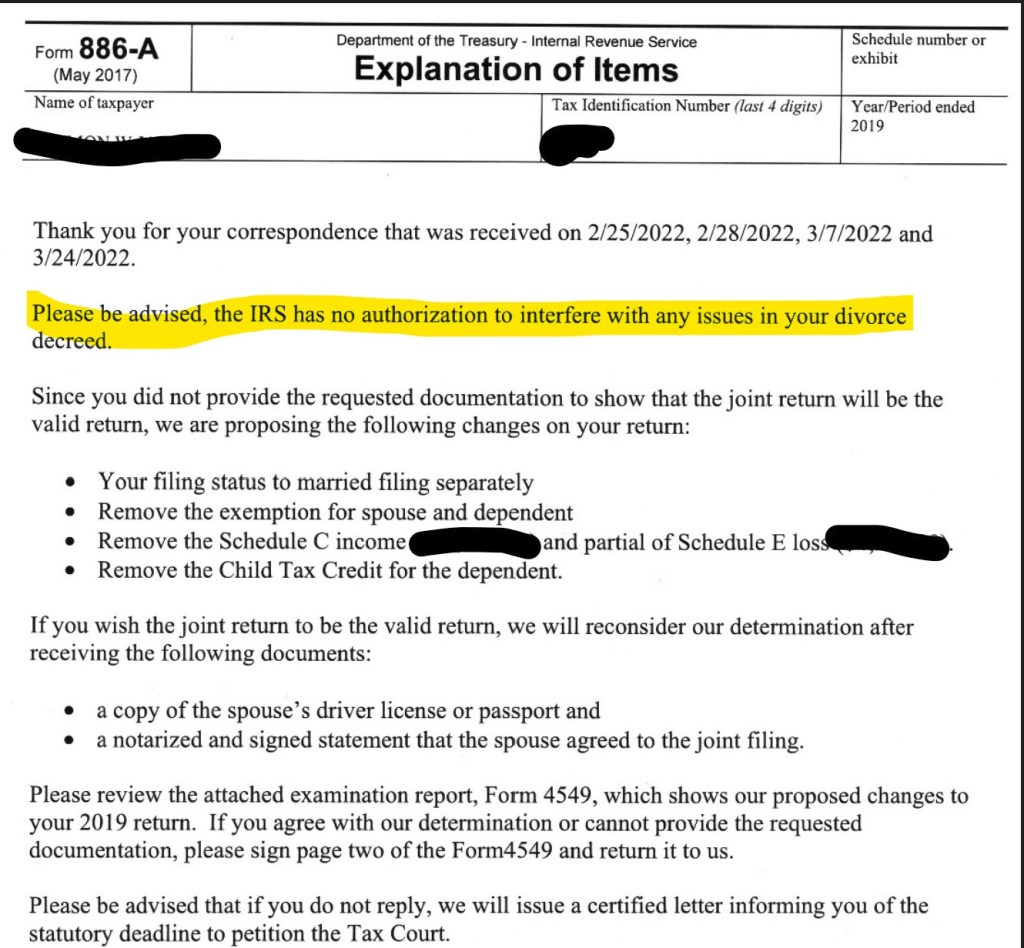

5) IRS Response Citing Divorce Decree Language (09/2022)What it shows: The IRS states it will not change its determination and cites specific decree language as part of the basis.

Why it matters: This becomes a key tension point in the record because the IRS rationale shifts toward reliance on decree language.

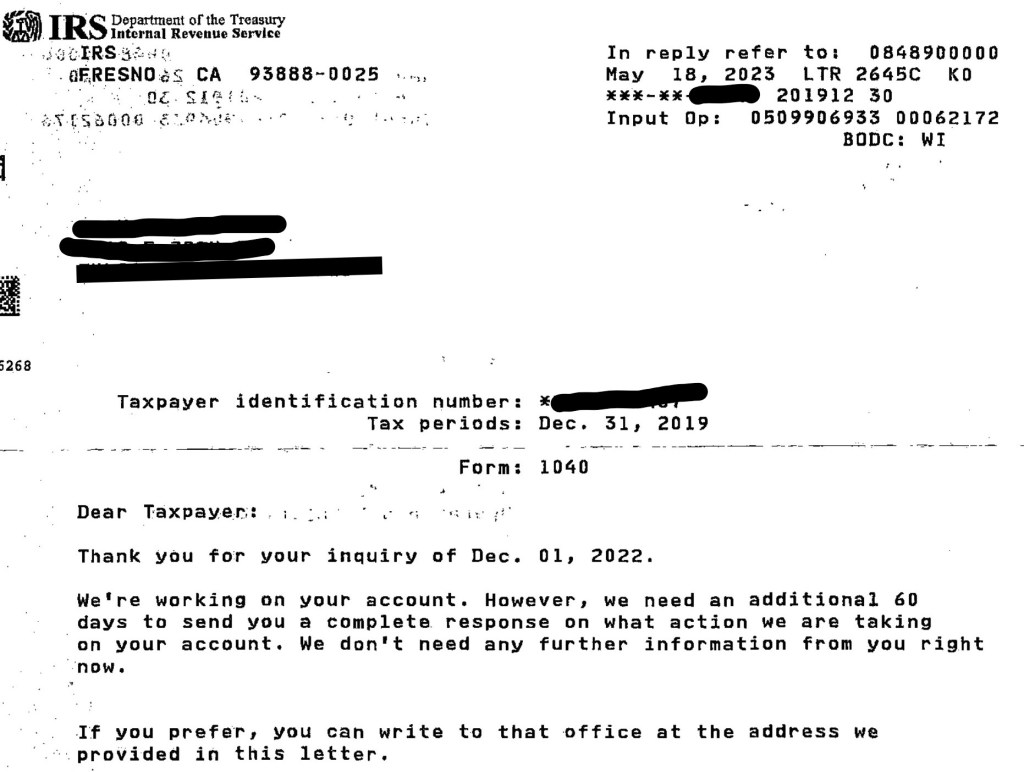

6) IRS “We Need More Time” Letter (60–90 day review notice)What it shows: The IRS says additional time is needed to provide a complete response and that no further information is needed from you right now.

Why it matters: This marks a period of delay and a lack of substantive follow-up while the case remains unresolved.

B) My Responses & Submissions to the IRS

These are the documents I submitted to challenge the determination and keep the record organized and evidence-based.

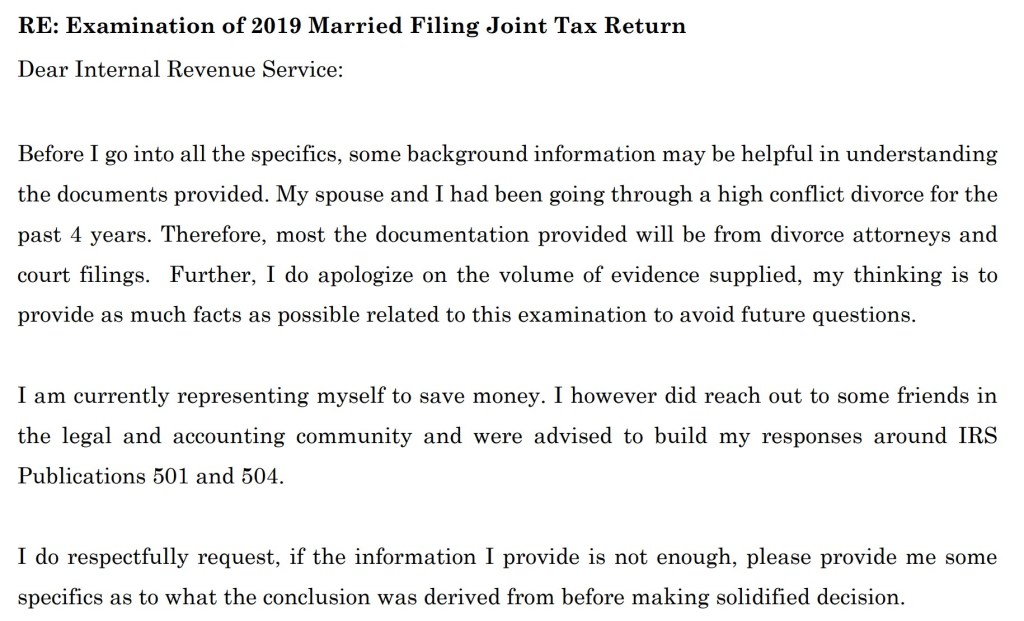

1) My Detailed Response Letter (02/2022)What it shows: A structured response to the examination, including exhibits and a clear request for fair review.

Why it matters: This is the foundation of my administrative record—what I said, what I provided, and what I asked the IRS to consider.

2) Submission Proof (Fax cover / transmittal)What it shows: Evidence of when and how the response packet was transmitted to the IRS.

Why it matters: Submission proof matters when disputes stretch over months/years and “receipt” becomes an issue.

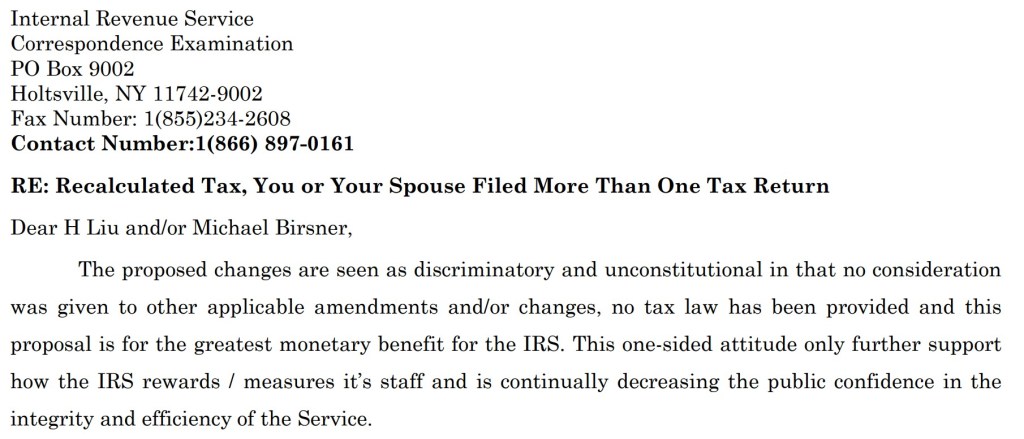

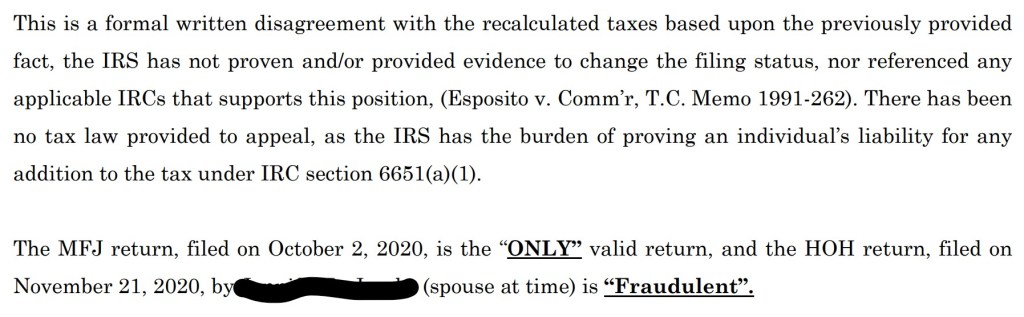

3) Formal Written Disagreement / Protest Letter (05/2022)What it shows: A direct disagreement with the proposed changes and a restatement of why the original joint filing should be treated as valid.

Why it matters: This moves the case from informal clarification to a clearly documented dispute posture.

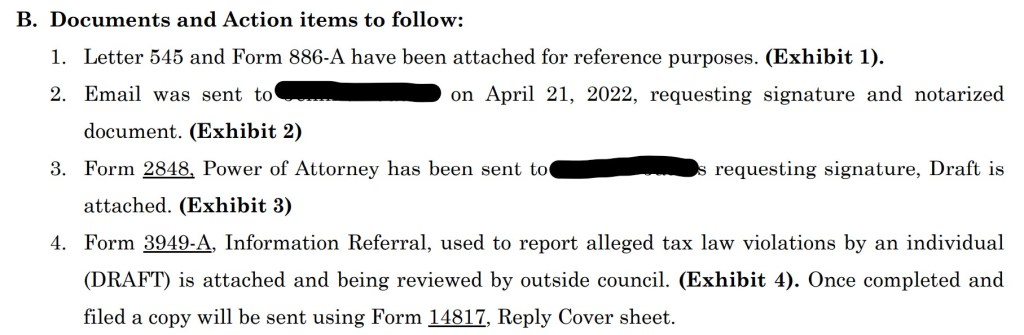

4) Information Referral (Form 3949-A)

What it shows: A procedural step recommended by professionals to ask the IRS to evaluate the conflicting filing directly.

Why it matters: This shows I used the channels the IRS provides to direct review to the root cause of the conflict.

Document image goes here

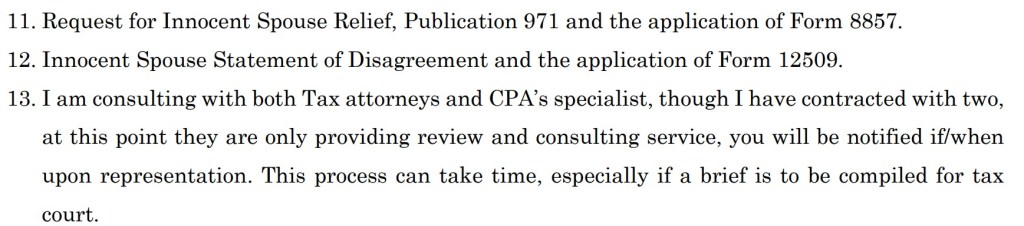

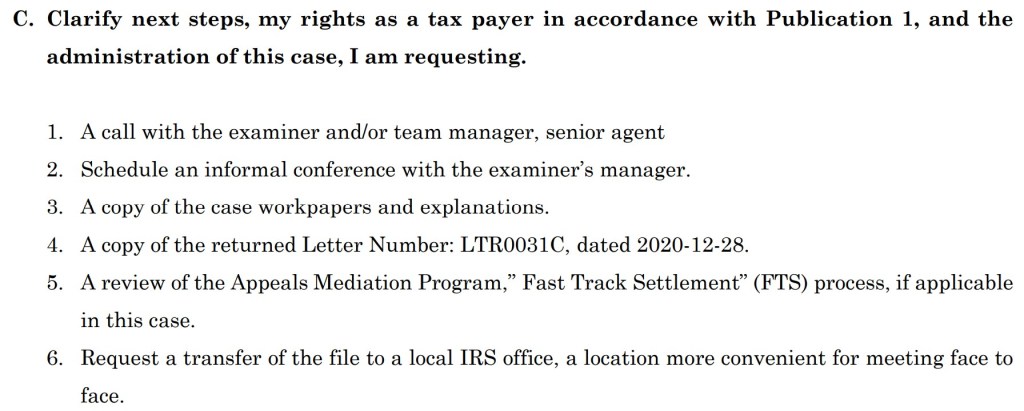

5) Audit Reconsideration Package (Cover letter + forms + exhibit list)

What it shows: A formal request to reopen and correct the determination, with forms and indexed supporting documentation.

Why it matters: This is the structured “reset” request asking the IRS to re-evaluate the determination using the correct standards and a complete record.

Document image goes here

C) Court Documents (Divorce Context — Excerpts Only)

These documents are included only to the extent they were referenced or relied upon in IRS correspondence or submissions.

1) Final Order (Tax-related excerpt)

What it shows: The court’s framework for how tax-filing issues were to be handled during the divorce process.

Why it matters: This provides context for how the filing approach was discussed and later evaluated.

Document image goes here

2) Divorce Decree (Dependency/tax benefits excerpt)

What it shows: The decree language about dependency claims/tax benefits that later appears in IRS reasoning.

Why it matters: This is part of what the IRS later points to when explaining why they did not change their determination.

Document image goes here

D) Collections & Urgency Documents

These documents show why the dispute is urgent and why representation matters now.

1) CP504 / Notice of Intent to Levy / Seize

What it shows: The collections escalation notice tied to the disputed 2019 tax period.

Why it matters: Collections actions can move faster than administrative review, creating pressure and risk of irreversible harm.

Document image goes here

2) Refund Offset Evidence (when posted)

What it shows: Evidence that a later-year refund was applied to the disputed 2019 balance.

Why it matters: This shows the dispute is not theoretical—money is being taken while the underlying dispute remains unresolved.

Document image goes here